")

[Updated on January 28, 2025 with updated screenshots from TurboTax Deluxe downloaded software for the 2024 tax year.]

You could have contributed to a Roth IRA after which realized later in the identical 12 months that you’d exceed the revenue restrict. You recharacterized the Roth IRA contribution as a Conventional IRA contribution and transformed it to Roth once more earlier than the top of the 12 months. Your IRA custodian despatched you two 1099-R kinds, one for the recharacterization and one for the conversion. This put up reveals you the way to put them into TurboTax.

In the event you had carried out the recharacterizing and changing within the following 12 months, you would need to break up the tax reporting into two years by following Cut up-Yr Backdoor Roth IRA in TurboTax, 1st Yr and Cut up-Yr Backdoor Roth IRA in TurboTax, 2nd Yr. Now since you caught the issue quickly sufficient earlier than the top of the 12 months, you possibly can deal with all of it in the identical 12 months by following this information.

Right here’s the instance situation we’ll use on this information:

You contributed $7,000 to a Roth IRA for 2024 in 2024. You realized that your revenue could be too excessive later in 2024. You recharacterized the Roth contribution for 2024 as a Conventional contribution. The IRA custodian moved $7,100 out of your Roth IRA to your Conventional IRA as a result of your authentic $7,000 contribution had some earnings. The worth elevated once more to $7,200 while you transformed it to Roth earlier than December 31, 2024. You obtained two 1099-R kinds, one for $7,100 and one other for $7,200.

In the event you didn’t do any of those recharacterizing and changing, please comply with our information for a “clear” backdoor Roth in How To Report Backdoor Roth In TurboTax (Up to date).

In the event you’re married and each you and your partner did the identical factor, it is best to comply with the steps under as soon as for your self and as soon as once more in your partner.

Use TurboTax Obtain

The screenshots under are from TurboTax Deluxe downloaded software program. The downloaded software program is extra highly effective and cheaper than on-line software program. In the event you haven’t paid in your TurboTax On-line submitting but, you should buy TurboTax obtain from Amazon, Costco, Walmart, and plenty of different locations and swap from TurboTax On-line to TurboTax obtain (see directions for the way to make the swap from TurboTax).

1099-R for Recharacterization

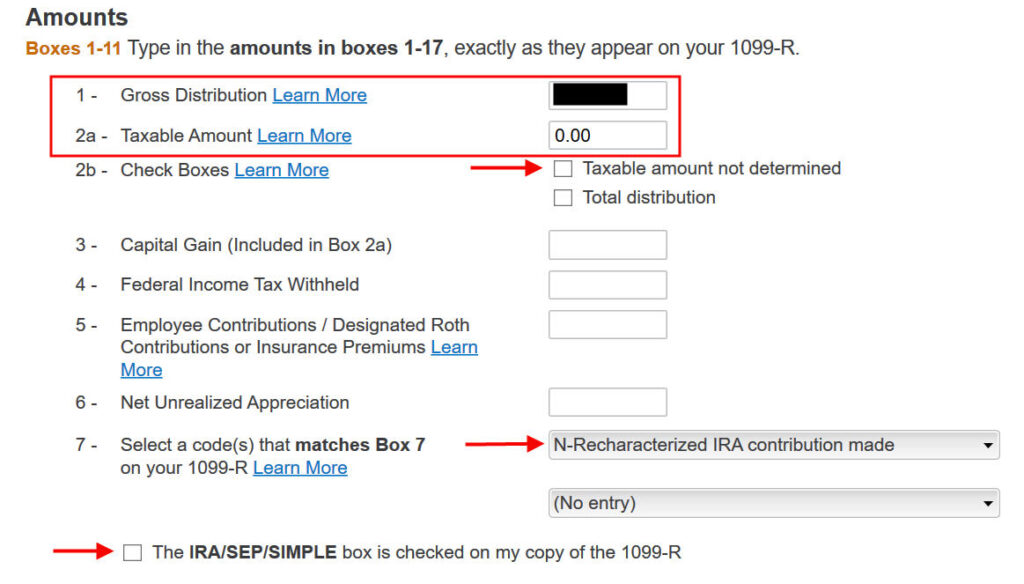

We deal with the 1099-R type for the recharacterization first. This 1099-R type has a code “N” in Field 7.

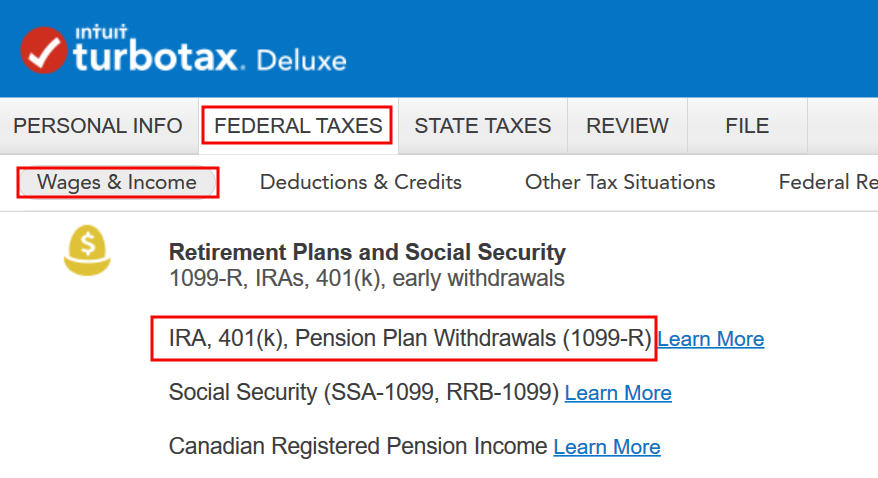

Go to Federal Taxes -> Wages & Earnings -> IRA, 401(ok), Pension Plan Withdrawals (1099-R).

Verify that you’ve obtained a 1099-R type. Import the 1099-R in the event you’d like. I’m selecting to kind it myself.

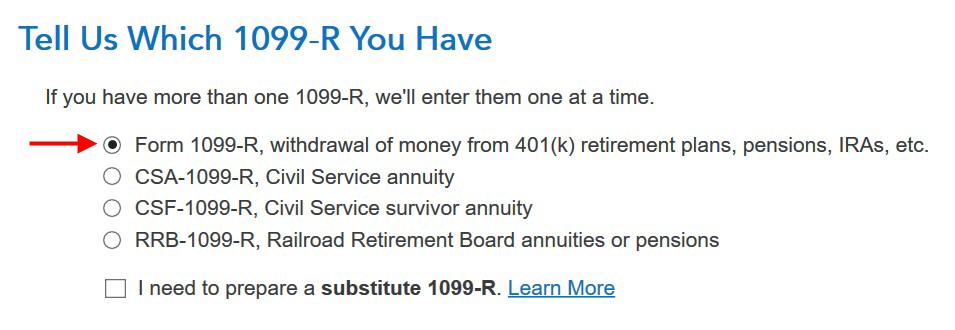

It’s a daily 1099-R.

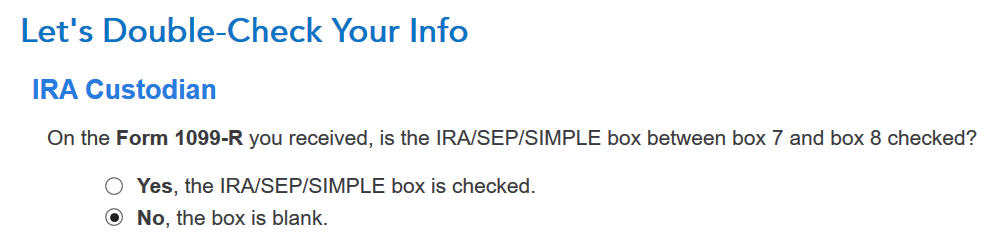

The 1099-R type for the recharacterization reveals the quantity moved from the Roth IRA to the Conventional IRA in Field 1. It’s $7,100 in our instance. The taxable quantity is 0 in Field 2a and the “Taxable quantity not decided” field isn’t checked. The code in Field 7 is “N” and the “IRA/SEP/SIMPLE” field might or is probably not checked. It isn’t checked in our pattern type.

That field is clean in our 1099-R, and that’s OK.

It’s regular to see zero in Field 2a and clean in Field 2b on this 1099-R type. TurboTax simply desires to double-check.

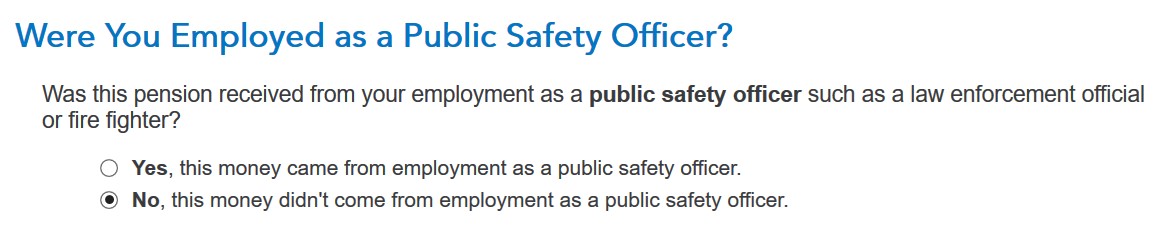

Not a Public Security Officer.

It wasn’t as a consequence of a catastrophe.

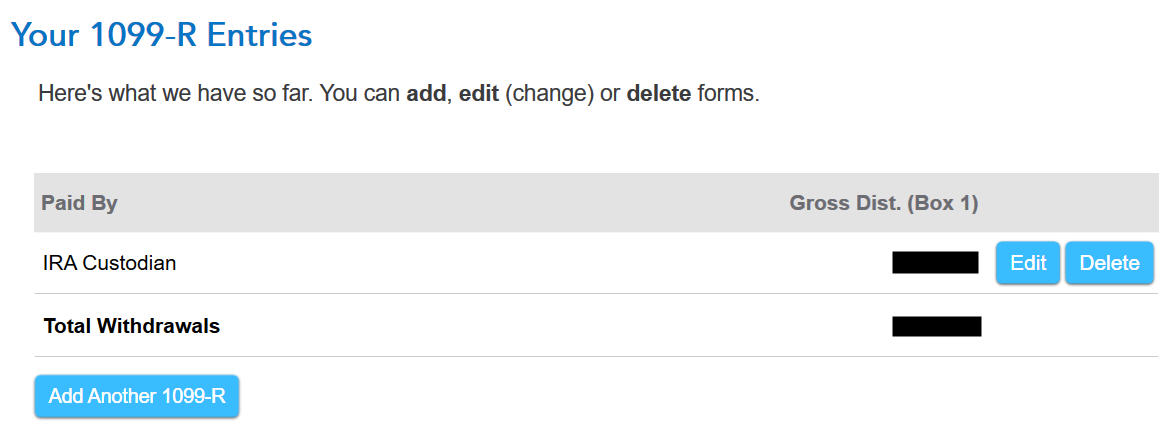

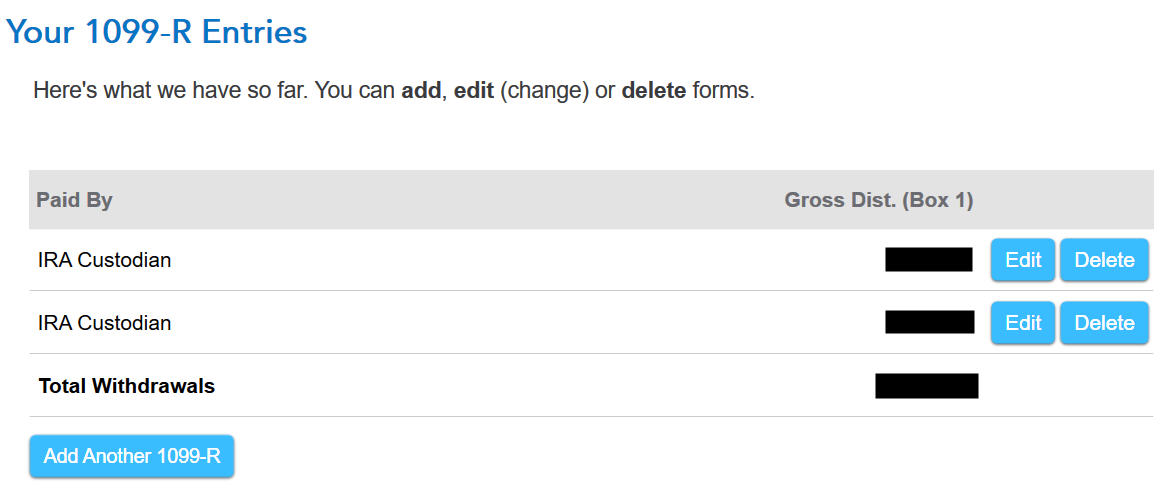

You’re carried out with the 1099-R type for the recharacterization. Click on on “Add One other 1099-R” so as to add the one for the conversion in the event you don’t have each 1099-R kinds imported already.

1099-R for Conversion

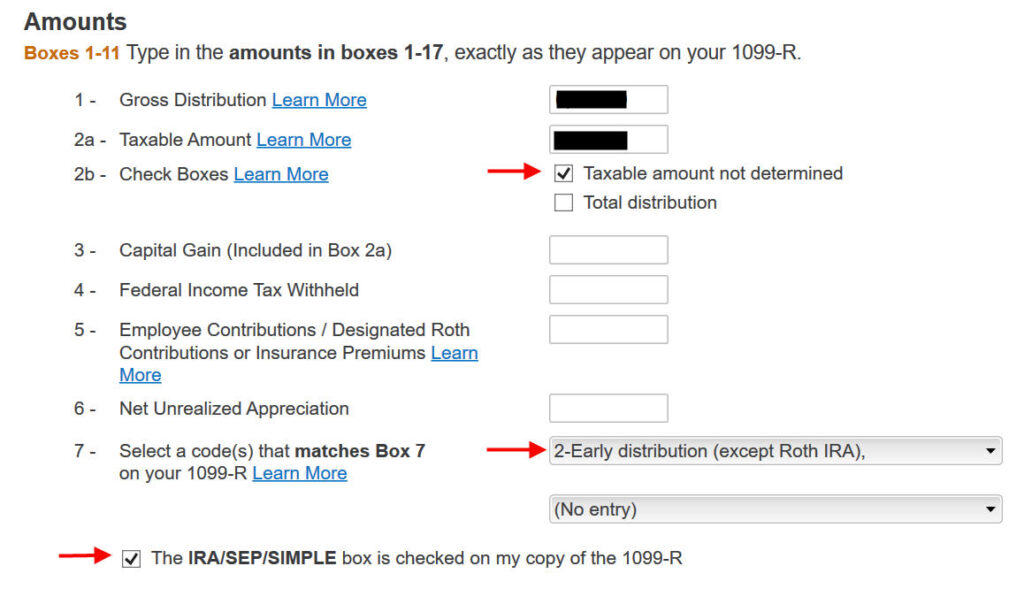

We enter the 1099-R type for the conversion now. This 1099-R type has a code “2” or “7” in Field 7.

This 1099-R type can be a daily 1099-R.

It’s regular to see the conversion reported in Field 2a because the taxable quantity when Field 2b is checked to say “Taxable quantity not decided.” The code in Field 7 is ‘2‘ while you’re beneath 59-1/2 or ‘7‘ while you’re over 59-1/2. The “IRA/SEP/SIMPLE” field is checked on this 1099-R type for the conversion.

It says that you simply don’t owe further tax on this cash however your refund meter drops. Don’t panic. It’s regular and solely non permanent.

It’s not an employer contribution to a Roth SIMPLE or a Roth SEP.

We didn’t inherit it.

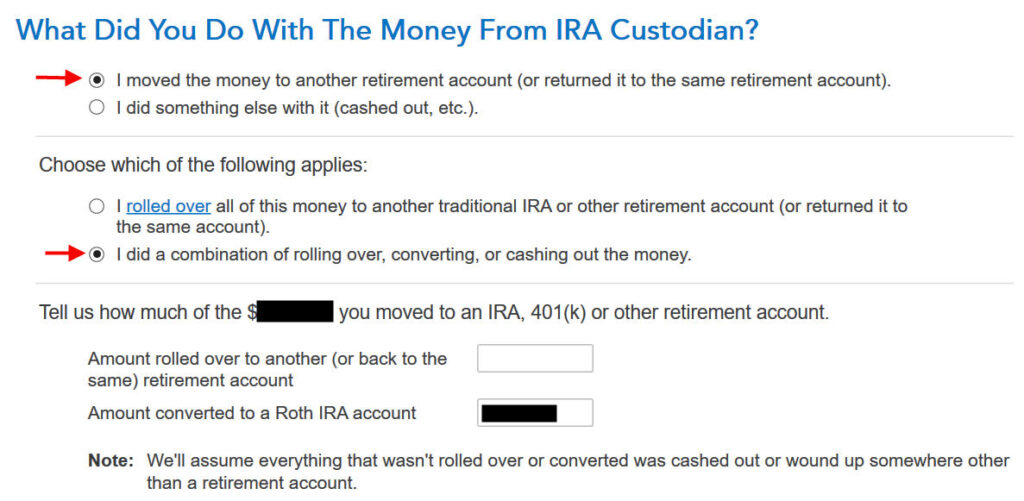

Transformed to Roth

First click on on “I moved …” then click on on “I did a mixture …” Enter the quantity you transformed to Roth within the field. It’s $7,200 in our instance. Don’t select the “I rolled over …” possibility. A rollover means Conventional-to-Conventional. Changing to Roth isn’t a rollover.

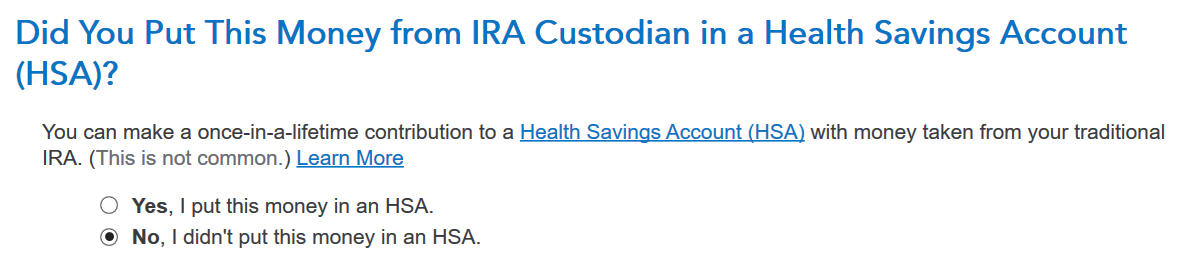

We didn’t put it in an HSA.

It wasn’t as a consequence of a catastrophe.

Now the 1099-R abstract contains each 1099-R kinds. Maintain going by clicking on “Proceed.”

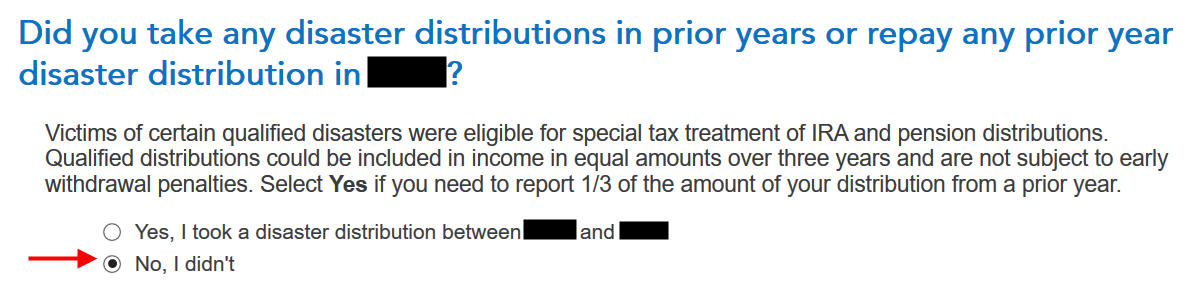

We didn’t take any catastrophe distributions.

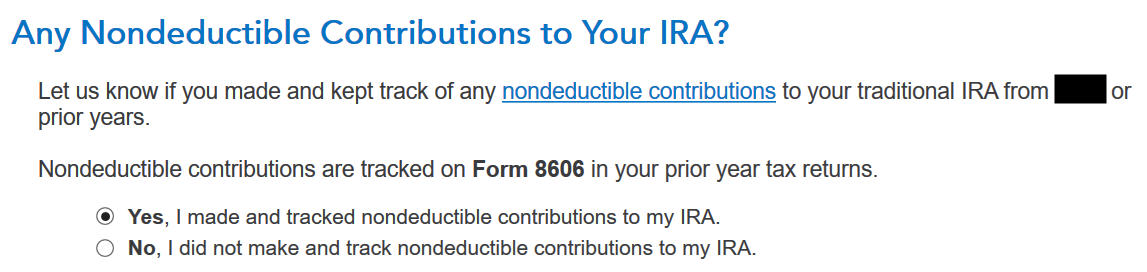

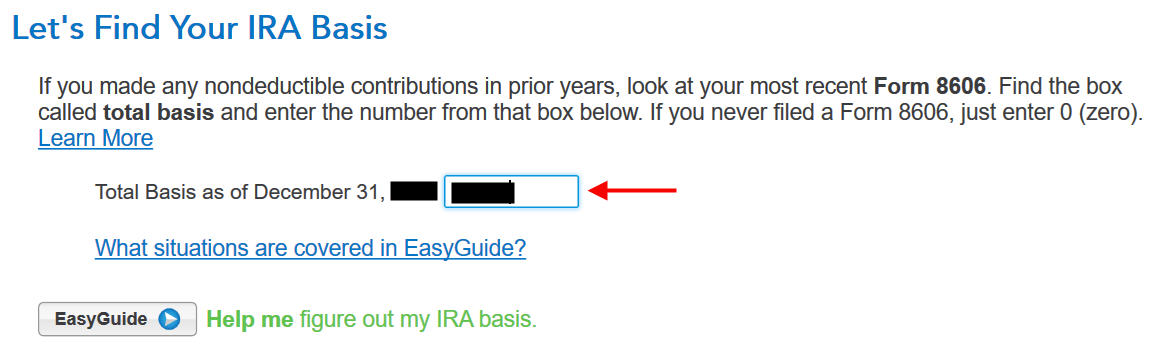

Foundation

You may reply “No” right here however answering “Sure” with a 0 has the identical impact and it means that you can right earlier mistaken entries.

This ought to be 0 in the event you hadn’t made any nondeductible contribution to a Conventional IRA earlier than. In the event you had, get the worth out of your final 12 months’s Type 8606 Line 14.

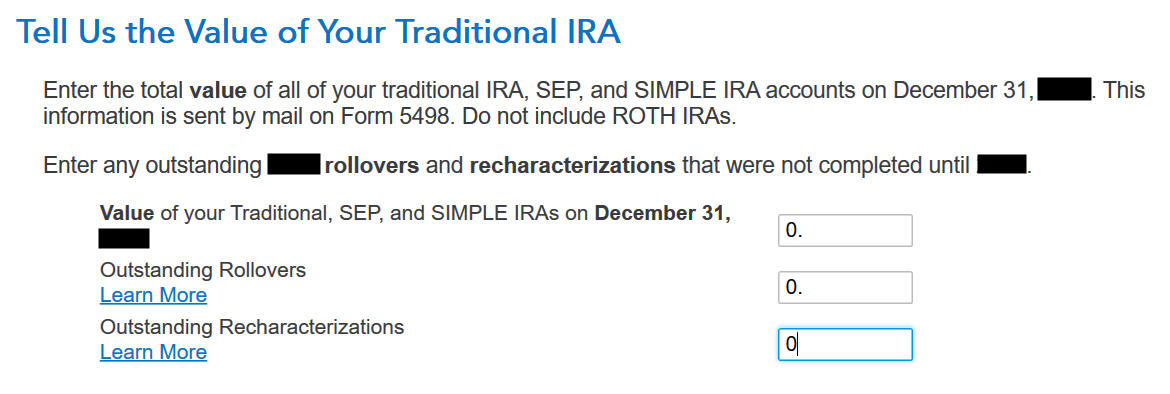

These are usually all zero in the event you transformed every thing. In the event you had a couple of {dollars} left within the account from earnings posted after you transformed, enter the worth out of your year-end assertion within the first field.

The refund meter remains to be briefly depressed. It’ll come again solely once we enter the recharacterized Roth IRA contribution.

Recharacterized Contribution

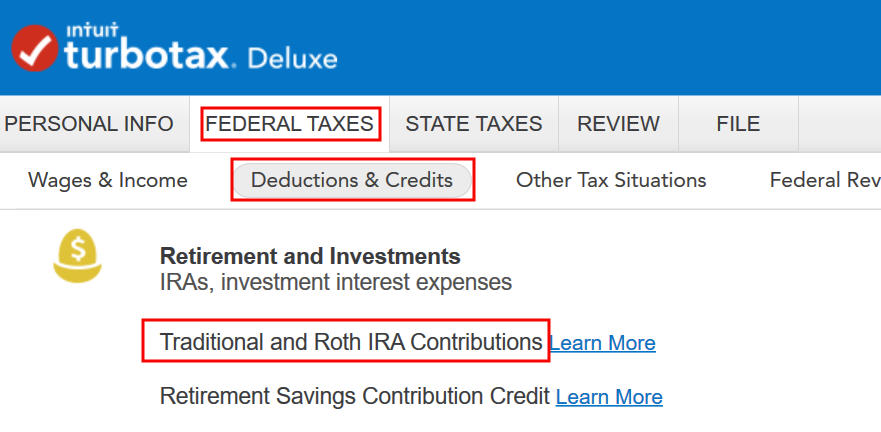

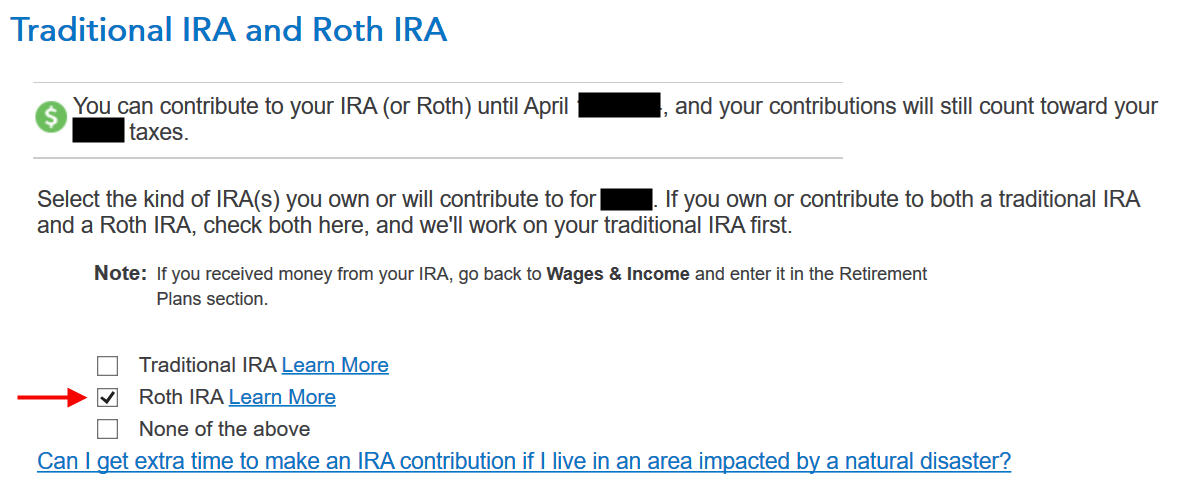

Go to Federal Taxes -> Deductions & Credit -> Conventional and Roth IRA Contributions.

Test the field for Roth IRA since you initially contributed to a Roth IRA.

We already checked the field for Roth IRA however TurboTax simply desires to ensure.

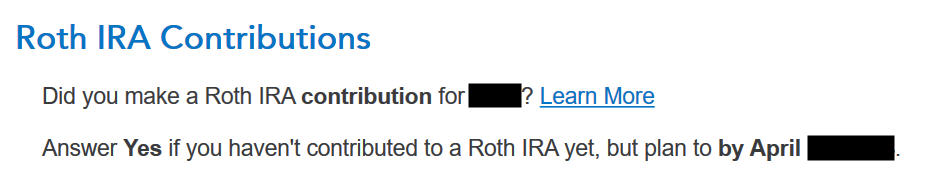

It was not a reimbursement of a retirement distribution.

Enter the quantity of your authentic Roth contribution. It was $7,000 in our instance.

Recharacterized

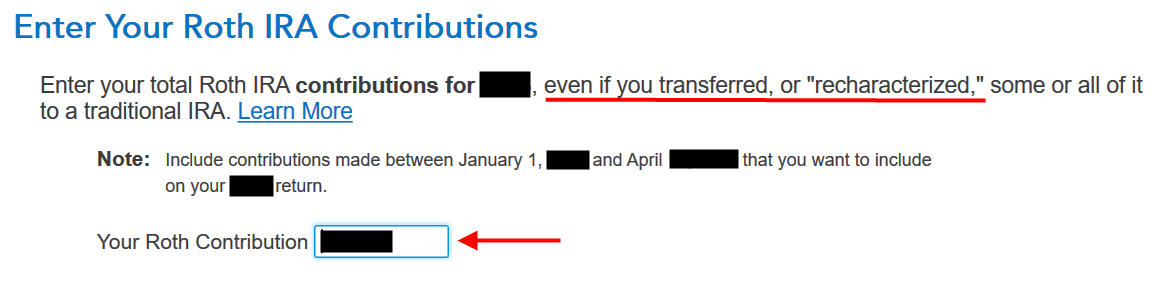

Now we confess that we recharacterized the contribution as a Conventional IRA contribution. Reply Sure right here.

The quantity right here is relative to the unique contribution quantity. In the event you recharacterized the entire thing, enter $7,000 in our instance, not $7,100 which was the quantity with earnings that the IRA custodian moved into the Conventional IRA.

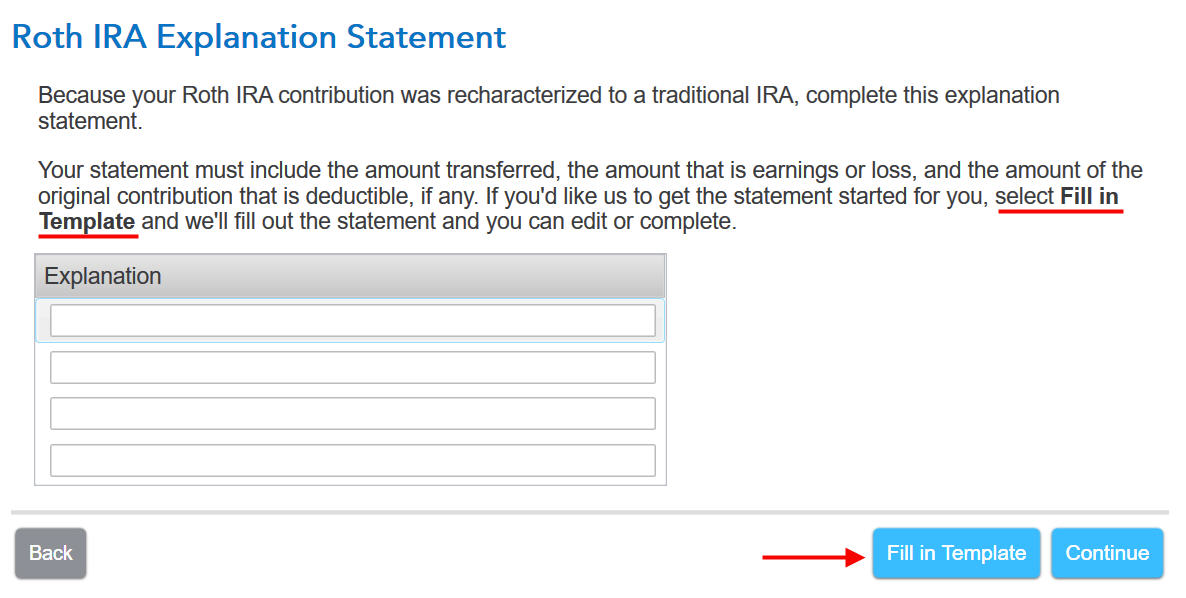

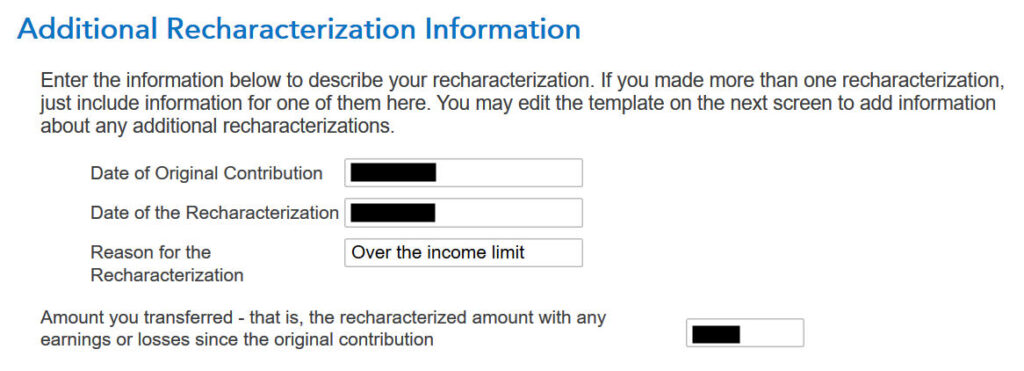

The IRS desires an announcement to clarify the recharacterization. Click on on “Fill in Template.”

Fill within the dates of your authentic contribution and your recharacterization. The quantity within the final field contains earnings. It’s $7,100 in our instance.

Roth Foundation

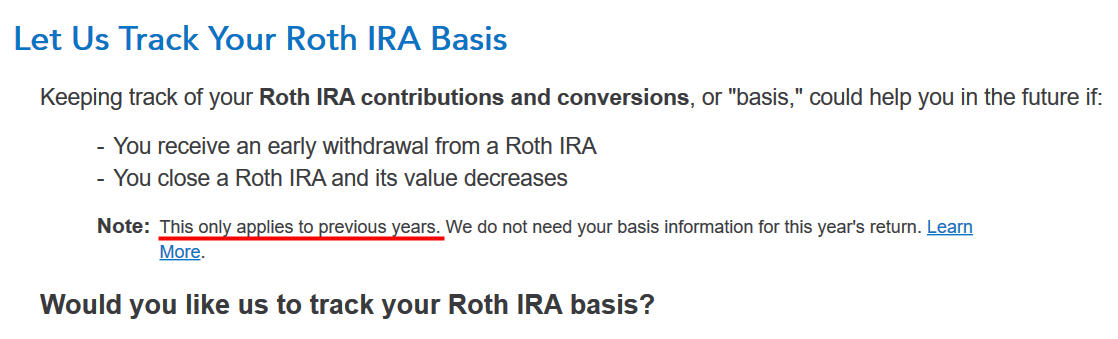

In the event you take up this supply from TurboTax to trace your Roth IRA foundation, it’s going to ask you questions on earlier years, which is extra hassle than it’s price to me. I answered No.

You don’t want to trace your Roth IRA foundation in the event you’re planning to withdraw out of your Roth account solely after age 59-1/2 and after you’ve had your first Roth IRA for 5 years. See Roth IRA Withdrawal After 59-1/2 in TurboTax.

We don’t have any extra contributions.

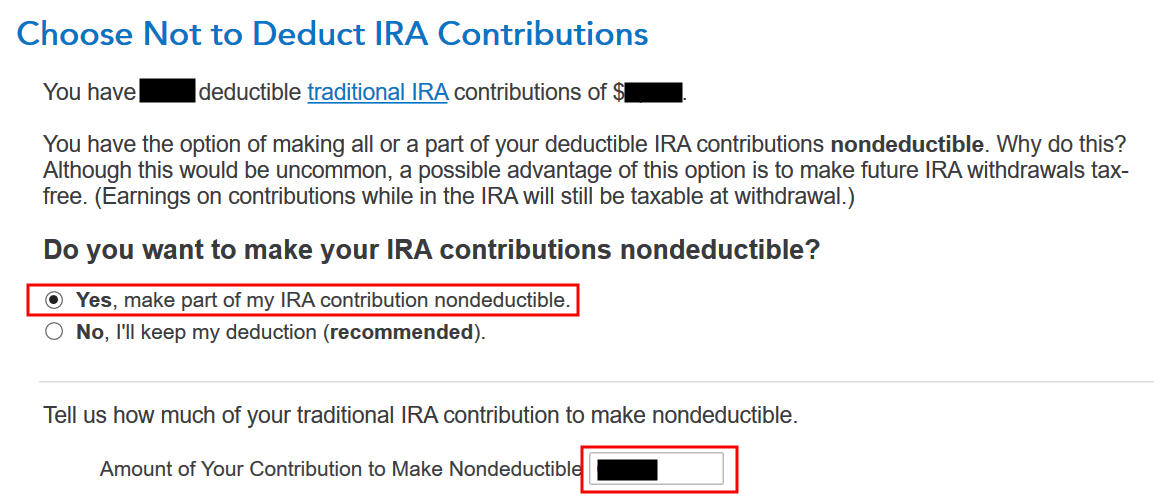

Make It Nondeductible

TurboTax reveals this solely when it sees your revenue qualifies for a deduction. You’ve gotten the choice to take the deduction or decline the deduction. Taking the deduction will make your conversion taxable, which can be OK as a result of it creates a wash. It’s less complicated in the event you make your full contribution nondeductible after which your Roth conversion isn’t taxable. Enter the quantity of your accessible deductible contribution within the final field. It’s $7,000 in our instance.

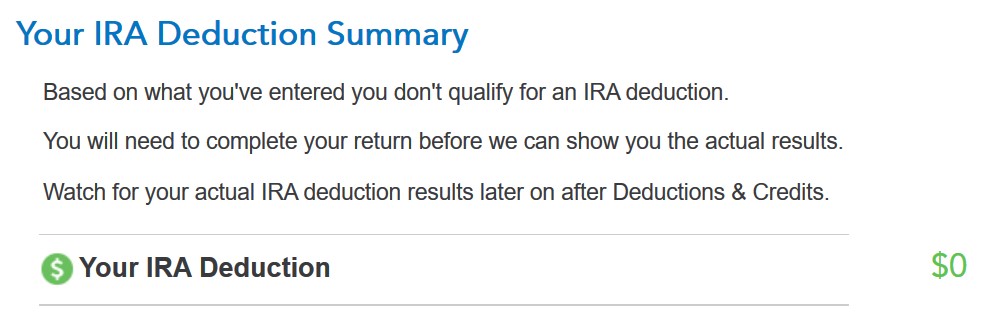

Your Conventional IRA deduction is zero, which is OK as a result of it makes your Roth conversion not taxable.

Taxable Earnings

Let’s take a look at how all these present up in your tax return. Click on on “Varieties” on the highest proper.

Discover Type 1040 within the left navigation panel. Scroll up or down on the proper to search out traces 4a and 4b. Line 4a reveals the sum of your two 1099-R kinds. It’s $14,300 in our instance. That is regular. Line 4b reveals that solely $200 is taxable. That’s the earnings between the time you contributed to your Conventional IRA and the time you transformed it to Roth.

Once you’re carried out analyzing the shape, click on on Step-by-Step on the highest proper to return to the interview.

Change to Clear Backdoor Roth

You averted having to separate your IRA contribution and Roth conversion in two completely different tax returns by recharacterizing in the identical 12 months and changing earlier than December 31. Nonetheless, you needed to do the additional work together with your IRA custodian and comply with all these steps on this information while you do your taxes.

It’s significantly better to go along with a “clear” backdoor Roth from the get-go. If there’s any chance that your revenue can be over the restrict once more, merely contribute to a Conventional IRA for 2025 in 2025 and convert it to Roth in 2025. You’re allowed to do a clear backdoor Roth even when your revenue finally ends up under the revenue restrict for a direct contribution to a Roth IRA. It’s a lot less complicated than the complicated recharacterize-and-convert maneuver. Then you definitely solely have to comply with our information for a clear backdoor Roth in How To Report Backdoor Roth In TurboTax.

Say No To Administration Charges

In case you are paying an advisor a proportion of your belongings, you’re paying 5-10x an excessive amount of. Learn to discover an unbiased advisor, pay for recommendation, and solely the recommendation.